The Ultimate Guide to Finance for Baby’s First Year

Congratulations, your precious baby is finally here. Now the real fun begins! While you may have purchased everything on your baby registry list, there are many family legal and financial tasks you cannot actually begin until your baby arrives, and some come with significant time sensitivity. So even if you’ve been preparing for a baby financially before he was ever conceived, you are likely now totally overwhelmed, sleep deprived, and can’t remember the last time you showered… and expected to handle legal and financial details.

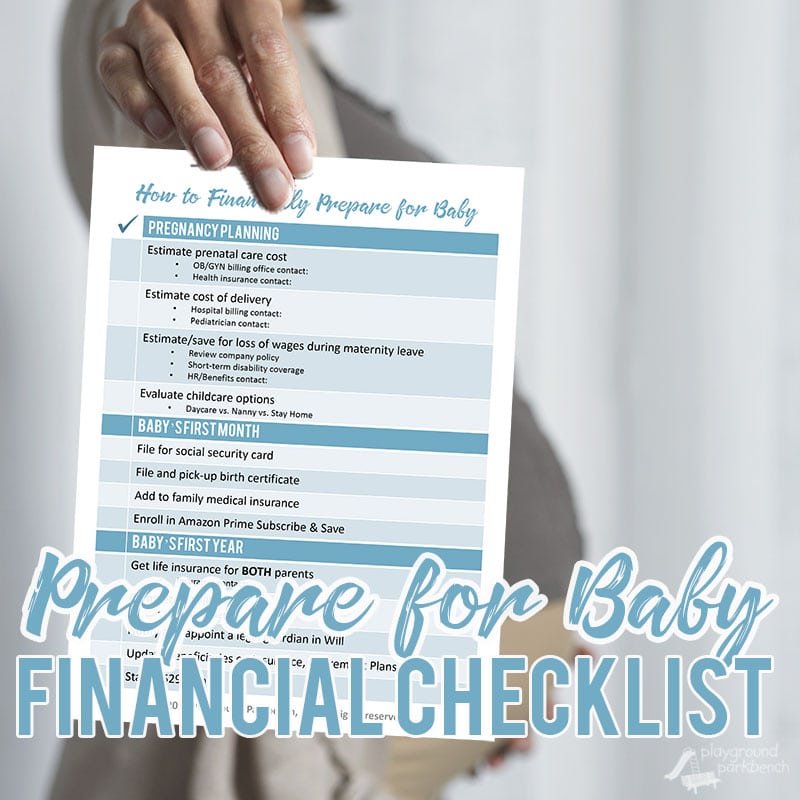

That’s where the baby financial checklist comes in – THE financial guide for all your must do’s for your baby’s first year. Grab your FREE printable baby financial checklist at the end of this post!

The Financial Checklist for Baby’s First Year

If you started with our preparing for baby checklist, you are off to a great start. But there are several legal and financial to-do’s you can’t really begin until your baby actually arrives. And some of these have to happen in the first 30 days after your child is born. I’ll cover each item in detail below, just as I did in part 1 – how to financially prepare for a baby – but be sure to download the FREE printable baby financial checklist at the end of this post to help you keep track of your to-do list.

Must Dos in Baby’s First Month

Before you have even left the hospital, some of these items will be brought to your attention. Every hospital and state operate differently, but at our hospital, a folder with boatloads of forms and information is ready and waiting the moment you are wheeled up from Labor and Delivery.

The two most critical forms you will want to be sure to take care of are the applications for a social security number and birth certificate. The other most time-sensitive matter is enrolling your baby in your health insurance plan, which must also be completed in the first 30 days.

Get Your Baby a Social Security Number

Nearly every step that follows will require having a social security number for your baby. It is your baby’s primary form of identification in the United States for the rest of their life. Your hospital should provide you with a birth registration form to complete and apply for a social security number. If you complete this at the hospital, they will submit it and you should receive your baby’s social security card in the mail in 6-12 weeks (though all my kids’ cards arrived much more quickly).

If for some reason they do not, or your baby is not delivered in a hospital, you can apply for one in person at your local social security office. You will complete paperwork there, and must also provide two documents proving your child’s identity, age and citizenship. This will likely be their birth certificate and medical records, bringing me to Must Do number two…

Pick Up Your Baby’s Birth Certificate

Upon delivery, you will also be given documentation to complete your child’s birth certificate. It will ask for things like your baby’s full name (so time to pick one!), and both parent’s names, birthdays and places of birth. In our State, the hospital submits this form and then we have to pick up the certified birth certificate from our local town secretary.

Once you have these two key documents, you want to store them in a safe and secure place. You will need to present them to register for daycare, preschool, athletic teams, summer camps and more. I highly recommend getting a fireproof storage box or safe

or safe to secure all these formal documents for your family.

to secure all these formal documents for your family.

Add to Health Insurance Plan

This is the biggest to do during your baby’s first month – missing this deadline can be very costly! Most health insurance plans have open enrollment periods at the end of every year. This is the only period you can make changes to your plan – like adding family members or changing coverage. However, they make exceptions for ‘life events’, such as births and marriage.

You have 30 days after a major life event to make changes to your policy – like adding your new baby to your family medical plan. You definitely want to be sure to do this, or they will reject coverage on your baby’s medical care. Contact your benefits provider or health insurance plan to add your baby as soon as possible. They will need your baby’s name, date of birth, and eventually their social security number as well once you receive it.

Enroll in Amazon Prime Subscribe & Save

Your single biggest financial shock in your baby’s first year won’t be the cost of delivery… it’s the cost of diapers. And if you choose feed your baby with formula, that’s even more expensive. After 3 kids and lots of research, the cheapest diapers I found were via Amazon Prime Subscribe and Save.

If you don’t use it already, it’s a no brainer once you have kids. You sign up for Prime, then set-up Subscribe and Save to deliver the things you need every month. You always save 20% off diapers, and can save up to 15% on your entire delivery by having at least 5 items delivered each month… diapers, wipes, diaper pail inserts, paper towels, formula or milk storage bags. It’s not hard to do… and you’ll save big money.

Related Post: 5 Ways to Stock Up on Diapers & Save

Legal and Financial To Do List for The Rest of the Year

After the first 30 days, you can pace yourself a little more. But you should still aim to complete the rest of this checklist during your baby’s first year.

Get Life Insurance

If you don’t have coverage already, you need it. There is a tiny human dependent on you for the next 18+ years – you want to make sure they are financially protected in the event something should happen to you or your spouse. And make sure you have life insurance coverage for BOTH parents, even if both parents are not working. Learn more about life insurance for parents, including how much coverage you need, here.

Even if you stay home with your child and have no income to replace in the event of your death, your surviving spouse will have to pay for childcare in your absence. It’s nothing anyone ever wants to think about, but do it. Term life insurance premiums are minimal and the financial security and peace of mind it provides is priceless.

Complete a Will & Appoint a Legal Guardian

Back in the camp of ‘things you don’t want to think about.’ But again, you are now responsible financially, legally, and emotionally for the care of a child. In the event anything should happen to you or your spouse, you want to ensure your child is cared for.

Discuss and agree on a legal guardian for your children to appoint in your will. And big to-do here – let that person know. It makes for good Hollywood movies to spring a kid on someone unexpectedly, but in the real world, you should let your siblings, neighbors, best friends know that you want them to take care of your children if anything ever happens to you.

Update Beneficiaries on Insurance, Retirement Plans

You likely did this when you got married, but this is a good time to double check again. Your will should also cover how your assets should be handled upon your death, but setting up proper beneficiaries on all your accounts will prevent any disputes. Your spouse should be your primary beneficiary, and children secondary.

Start a 529 Plan

Just like saving for retirement, the earlier you start saving for college, the more money you will save and earn interest on (learn more about the magic of compounding). The last item on your baby financial checklist is to start a college savings plan, known under our tax code as a 529 plan.

A 529 Plan is a savings account for college. You can contribute unlimited after tax dollars to the fund, which will accrue interest and capital gains tax-free. So long as the funds are used to pay for college, all earnings will remain tax-free. Some states, like our state of Connecticut, offer plans which allow state income tax credits to a state approved 529 Plan. Other college savings plan may offer matching programs for contributions during your baby’s first year of life. All the more reason to get it started early.

Download Baby Financial Checklist

I wouldn’t expect any new mom, under the stress of sleep deprivation and recovery from child birth to remember all of this (or any of it)! So be sure to visit part 1 in this series, How to Financially Prepare for a Baby, to download and print the FREE How to Financially Prepare for Baby Checklist.

How did you financially prepare for your new baby? Do you have questions or concerns about any of the checklist items above? Feel free to email me your Family Finance questions or ask them on my weekly Money Talks chat on Instagram. They may just be the inspiration for our next Family Finance post.

Need to remember this? PIN IT!

[…] Family Financial Savvy […]

[…] Family Financial Savvy […]

[…] The Baby Financial Planning Checklist covers pregnancy, steps for your baby's first month and first year. Find the detailed explanation for the steps post your babies birth in part 2 of this series, The Ultimate Guide to Finance for Baby's First Year. […]

[…] of the major items on my First Year Financial Checklist for parents is putting a will in place to protect and provide for your children in the event […]