How to Financially Prepare for Baby

There are countless baby registry checklists you can find across the internet. But what is harder to find is a checklist that outlines how to prepare for a baby financially. Are you expecting or starting to plan your family? Grab your FREE printable checklist - How to Financially Prepare for a Baby - at the end of this post.

Baby Financial Planning

Babies are expensive - from medical bills and potential loss of income to maternity leave, to daycare, diapers and formula. But beyond that, for most parents, it is the first time in your life you have financial responsibility for another human. This goes beyond providing for just their immediate basic needs - but also planning for their futures.

Financial Planning During Pregnancy

Whether you are already pregnant or just thinking about starting a family, these first financial preparation steps are arguably the hardest on the list. Why? Because they mostly involve medical care, insurance coverage and the unknown. This checklist will walk you through how to best estimate medical costs, as well as prepare for the future impact to your monthly income from maternity leave and childcare costs. In the early days of your pregnancy, you should focus on estimating future medical costs, determining your benefits coverage for maternity leave, and as your pregnancy progresses, begin evaluating child care options.

Estimating Pre-Natal Care Costs

After three near normal pregnancies, all with the same obstetrician, with the same insurance provider, I honestly found trying to get clear answers to medical costs and coverage during pregnancy the most frustrating health care experience of my life. EVERY time. Your OB will recommend procedures, blood tests, and ultrasounds, and you will ask a simple question like - "Is it covered by my insurance?" or "How much does that cost?" And nearly 100% of the time the answer will be "I don't know." WHAT??

Your first pre-natal appointment typically occurs after 6-8 weeks. First and foremost, make sure your doctor is an approved provider under your insurance AND make sure the hospital they deliver at is too. Before you go, ask for the contact information for the billing office or department of your obstetrician's office. Write it down on the checklist - you will call it more than once. Similarly, write down the number of your insurance provider for claims or customer care. Review your insurance policy and understand what your annual deductible amount is.

[click_to_tweet tweet="Deliver a baby late in the year... make the most of your annual medical deductible! #familyfinance #newmom #babyprep'" quote="Deliver a baby late in the year... make the most of your annual medical deductible!" theme="style3"]

At your first appointment, your doctor will outline what standard care is in the practice for pre-natal care, including frequency of visits, tests and ultrasounds. Typically, the billing office can give you the out-of-pocket cost for your pre-natal care based on standard care and your specific insurance coverage. If they recommend anything that deviates from this, call the billing office and request the medical billing code associated with the treatment or service. Next, call your insurance provider, give them the code and ask if the procedure is covered and/or what your out-of-pocket cost will be.

Family Finance Mom Tip: Having a baby with a Fall due date can save you money. All of your medical and delivery costs will occur in a single calendar year, and thus, a single year's medical deductible. Delivering in the first half of the year leaves you under two year's worth of deductibles, and potentially as much as twice the out of pocket cost.

Estimating Delivery Costs

Here's where pregnancy often becomes less predictable. Again, contact your OB's billing office and your insurance provider to determine the out-of-pocket costs of a vaginal delivery and/or a c-section. Do you plan to have an epidural? That gets billed by a different provider, the anesthesiologist, at the hospital, not your OB's office.

Your baby will also be visited by the pediatrician at the hospital. When you select a pediatrician, make sure they are an approved provider under your insurance coverage AND that they are an approved provider at the hospital or facility where you will deliver. You will be billed for your hospital stay, the baby's hospital stay, delivery and postpartum care by your OB, any anesthesiology services, and visitation of the baby by the pediatrician at the hospital prior to discharge. If you have a boy and elect to have him circumcised, you will be billed for that as well.

If everyone is healthy, that's where the big medical costs end. As an example (or three), with all three of my children, I had vaginal deliveries, with an epidural. I delivered with the same practice, same hospital and same pediatrician. With my second, I had a brief hospital visit with kidney stones around 7 months, and with my third, I was taken by ambulance from my last OB visit and induced, but otherwise, no unusual medical care.

Without insurance, it would have cost approximately $45,000 for EACH child. Insurance companies negotiate better rates - their cost was approximately $20,000 for my first, $22,000 for my second (extra hospital visit) and $25,000 (ambulance, induction and circumcision) for my third. With each delivery, we paid approximately $2,000-2,500 in out-of-pocket costs for pre-natal care and delivery. Note, this can vary widely based on your insurance coverage, deductible, medical needs, and timing.

Estimate Income Impact from Maternity Leave

If you are in the planning stage (pre-pregnancy), review your benefits and company maternity leave policy. FMLA mandates certain employees receive 12-weeks of unpaid, job-protected leave annually with group health benefits maintained for certain family and medical reasons. There are some catches - like your company must have more than 50 employees and you must be employed for 12 months before taking leave. Your company policy has to minimally meet FMLA, but may be better.

[click_to_tweet tweet="Planning a family? ST disability insurance can cover unpaid maternity leave #familyfinances #newmom #insurance' " quote="Planning a family? ST disability insurance can cover unpaid maternity leave" theme="style3"]

If you are not already pregnant, you may be able to sign-up for short-term disability insurance through your company benefits provider. Typically, you can only enroll during the open enrollment period every December, and you must have coverage PRIOR to being pregnant. But ST disability coverage can cover lost wages during maternity leave in the event your leave is unpaid.

Evaluate Child Care Options

Once you are pregnant, if you plan on returning to work, you will want to begin looking for childcare options relatively early in your pregnancy. Most reputable care providers due to caregiver-to-infant ratio restrictions have very limited openings and waiting lists by month. Monthly daycare costs can vary greatly depending on where you live, but in many places, childcare, especially if you have more than one child in daycare, can rival the monthly cost of rent or your mortgage.

When we were evaluating day care options before my oldest was born, it was clear even just trying to make scheduled visits, that daycare was not going to work for us. My husband and I both worked in finance with long hours. No way was I going to make it to pick-up my child by 5:30PM every day. We hired a nanny at a hefty premium to daycare to match our long work hours. She wanted a raise before she even started due to her own unforeseen costs, and we began to evaluate whether my going back to work even made sense financially.

While this is not strictly a financial decision, you should evaluate the cost of childcare after taxes, commuting costs, dry cleaning and other work-related expenses and determine if paying someone else to take care of your children makes sense financially. If you think you can't afford to stay home and want to - lay out the math. With small lifestyle changes, you might be surprised what you can make work for your family.

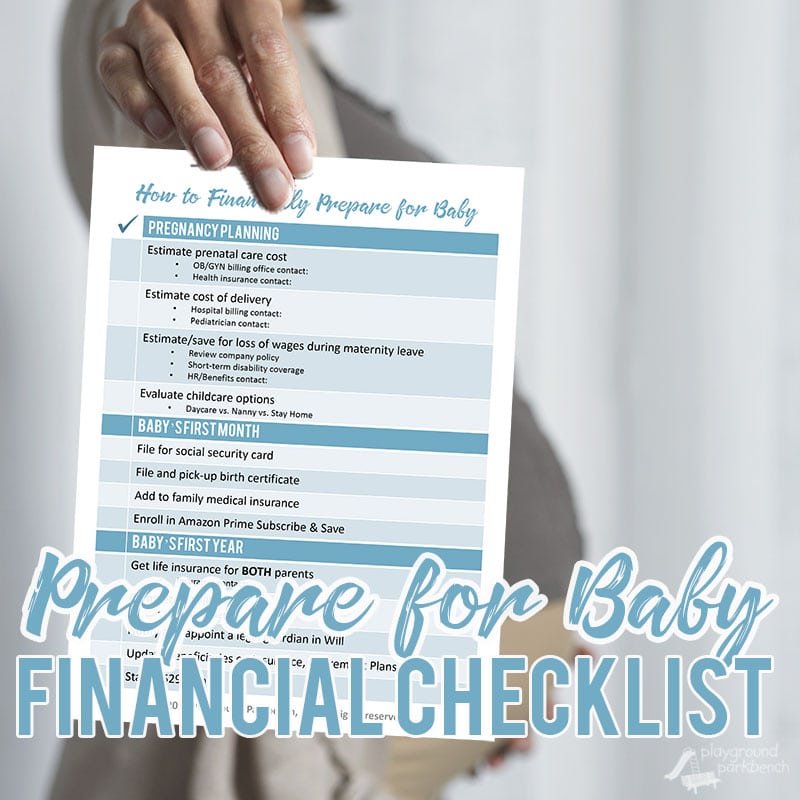

Grab Your How to Financially Prepare for Baby Checklist

You can download your FREE printable Baby Financial Planning Checklist below.

The Baby Financial Planning Checklist covers pregnancy, steps for your baby's first month and first year. Find the detailed explanation for the steps post your babies birth in part 2 of this series, The Ultimate Guide to Finance for Baby's First Year.

Get the Baby Financial Planning Checklist

Click below to access it from the

FREE Family Finance Mom library.

Here you will find the FREE printable PDF with everything you need to do to financially prepare BEFORE your baby comes and through their first year.

Save this for later... PIN THIS!

[…] Family Financial Savvy […]

[…] Family Financial Savvy […]

[…] your baby arrives, and some come with significant time sensitivity. So even if you’ve been preparing for a baby financially before he was ever conceived, you are likely now totally overwhelmed, sleep deprived, […]