This Week’s Stock Market News 4-19-2021

Welcome to earnings season… if the first two weeks of April were relatively quiet, last week was anything but as Q1 2021 earnings season got underway with more than 100 companies reporting results. Mostly solid earnings reports, as well as a little more softening of interest rates led a widespread, market rally. On the not so good news front? CPI numbers for March are in… and inflation is up, as predicted. For more finance news, you can find all the previous Monday Market Update’s here. You can now also get the finance news of the week every week on Finance Explained, my new podcast, along with a deep dive on a topic relevant to the week’s headlines.

Monday’s Finance News of the Week

The overall market sentiment thorughout 2021 continues to be driven by two key themes, and last week, was no exception:

- Stock market rallying on hopes of recovery

- But tempered by rising interest rates fueled by inflation concerns

Last week, the start of earnings season brought solid earnings reports giving solid data points of the recovery solidly underway, while interest rates continued to soften from their early April highs, giving the market room to run, with all indices and sectors showing solid gains for the week. Note the large upside surprises to earnings from the major banks. This is largely due to reversals of reserves they took a year ago, in preparation for rising delinquency rates on their loan portfolios during the pandemic. To date, these have not materialized to the degree anticipated, so they are now reversing them, which positively impacts earnings in the current quarter, but are typically normalized out of earnings by analysts given they are not part of ongoing operations.

The S&P 500 closed at a new all-time high Friday, for the third week in a row. The market finished the week up +1.4%, and is now up +11.4% year-to-date. Tech and growth stocks continue to outperform with softening interest rates, and the Nasdaq was up 1.4% and Growth stocks up 1.8%, after underperforming with rising interest rates for most of the start of the year.

With the down-tick in interest rates, we also saw 30-year mortgage rates tickdown as well, after nearly 2 months of increasing, now at 3.04%, down 9.0bps from the week prior, and still near historic lows.

I still believe interest rates softening over the last two weeks is just a temporary pause – not a trend expected to continue – given growth and inflation expectations. We are still seeing inflation expectations in the 10 Year Treasury to TIPS spread, and this month’s just released CPI numbers for March give us hard data confirming those expectations are valid. Ten-year TIPS yields are currently negative, meaning current actual long-term interest rates are lower than expected inflation. The Treasury spread to TIPS continues to hold steady well above 2%, ending last week at 2.30%. This spread historically has predicted inflation growth about a quarter ahead of time, and at current levels, estimates inflation of about 2% for the coming quarter (vs. latest level for March of 2.6%). It should be noted the Fed’s own estimates for 2021 inflation now sit at 2.4%.

Last Week in the Markets

Last week, the pause in rising interest, as well as the mostly solid Q1 2021 earnings reports from the first round of corporate earnings drove a widespread stock market rally. Hundreds more companies are scheduled to report earnings this week as well – so expect there to potentially be volatility in individual names as company’s report.

While for most of 2021 we’ve seen recovery hopes and inflation concerns drive outperformance of cyclical, small cap and value stocks over growth and tech stocks, we’ve seen a shift the last few weeks. Growth and tech stocks rallied for the third week in a row, up +1.8% and +1.4% for the week, respectively. This month’s growth and tech rally accounts for the entirety of their year-to-date index performance. But we’ve really seen a broad market rally over the last two weeks, with all indices and sectors posting strong, positive performance, save Energy, which has been in a bit of a holding pattern.

In the bond market, you can see a similar outperformance of higher risk securities year-to-date, as investors have sought higher sources of return. High Yield bonds, with lower credit and higher interest rates, have significantly outperformed Investment Grade and Treasury bonds year to date, though all bond indices are mostly flat to down year-to-date, as rising yields drive prices down. As mid-to-long-term rates have softened in over the course of April, we’ve seen bond market performance take a bit of a pause. For more on the inverse relationship between bond yields and bond prices, see 10+ Different Types of Investments under How Bonds Work.

Mid and long-term bond yields peaked at the start of April, and you can see the difference in the yield curve today vs. 2.5 weeks ago above. Just that little bit of softening, mostly due to investors’ beliefs that the Fed will hold off on raising rates for now, has given the market room to run over the last 2-3 weeks.

The rise in the longer-term end of the current yield curve since the start of the year has driven the price of bonds down significantly year-to-date. The more steeply upward sloping yield curve is representative of a more normal, growing economic environment, but also a result of inflation expectations and expectations of more government borrowing in the short-term. Compare it to the yield curve last March, an inverted curve, when long-term Treasury rates hitting their lowest levels ever, which is predictive of a recessionary environment.

Concerns over inflation, and the rapid growth in the money supply, have fueled the rise in more speculative investments, like commodities and cryptocurrencies, like Bitcoin. Want to know more about what’s driving inflation concerns? Check out this post on Higher Inflation.

One developing story over the weekend and early Monday is a sell-off in cryptocurrency, which doesn’t yet appear in the charts below through Friday. Experts are calling it a flash crash, but Saturday, Bitcoin sold off by more than 14%, on speculation that countries around the world are about to increase regulations and/or ban cryptocurrencies entirely. Increased regulation is anticipated by the US Treasury Department, though the timing is still unclear. Many countries are also launching or evaluating the launch of their own digital currencies, including China, England and the US.

The Economic Weekly Market News

This week’s major economic releases included:

- Tuesday: Consumer Price Index for March

- Thursday: Advanced Retail Sales for March, Weekly Jobless Claims, Mortgage Rates & Fed Balance Sheet Data

Consumer Price Index for March

We have been tracking closing tracking indices for inflation as concerns about higher inflation have increased. The Consumer Price Index (CPI) for March was released last week, and now clearly shows the inflation we have all been anticipating.

Over the last 12 months, weak energy comparisons have served to offset increasing prices in other sectors like Food. But from here forward, as long as energy prices remain where they are or increase, they will continue to serve as a tailwind, driving inflation. It’s important to realize also that energy prices impact far more than just your utlity bills or the gas you put in your car. They add to the cost of almost all consumer goods due to rising transportation prices, as an example.

The Fed now uses the PCE Price Index for their official measure of inflation. Its March values will be out April 30th. The Fed has said it targets 2% long-run average inflation – and given it has run below 2% over the last year, they will allow it to run above 2% for a period of time before raising interest rates, particularly given other objectives, like full employment,

Advanced Retail Sales for March

The US Census Bureau releases an estimate of US retail and food services sales each month. Why do these matter? They give us the first indication each month of how consumer spending is doing, and recall that consumer spending represents 70% of our overall economy.

We expected Retail Sales to be strong, fueled by the third round of stimulus checks that went out last month. And they were – up +9.8% vs. February, on a seasonally adjusted annualized basis. If you zoom in at the most recent data, you can see how stimulus checks boosted January spending above the long-term trendline, February was just coming back towards reality, and another round of stimulus in March boosted sales again.

Sales were up nearly 10% or more vs. February in all major categories, save Grocery Stores. One of you asked me how that’s possible given rising food prices. It’s basically a shift back towards restaurants as restrictions lifted in many states, so absent food price increases, grocery store sales would likely be negative. On a year over year comparison, growth levels are extreme – remember, this is comparing stimulus-boosted March 2021 numbers vs. half a month of total lockdown in March 2020.

Remember, the US issued more than 90 million checks worth a total of $242 billion in March. That in combination with accelerating vaccination rates, and many states easing back health restrictions, is driving a healthy recovery in retail spending. Let’s see how the trend continues into 2021, absent further stimulus.

Weekly Jobless Claims

While the monthly employment report gives us far more insights into demographics and industry breakdowns of the labor market, Weekly Jobless Claims gives us more real-time data on the labor market’s progress. On Thursday, weekly jobless claims for the week ending 4/10 dropped to 576,000, a decrease of 193,000 from the previous week’s revised level. This is a good sign, but I want to see these lower levels continue to drop for several weeks before I say we are truly seeing continued labor market recovery – which has mostly been stalled since November.

Total insured unemployment, under regular state programs, is down to 3.7 million people, an insured unemployment rate of 2.7%. However, this remains only a fraction of those covered under the expanded pandemic and emergency programs at both the state and federal level.

Total insured unemployment under these programs for the week ending 3/27 (this comes at a longer lag) is far greater – 16.9 million, this week down by 1.2 million Icontinued claims vs. the week prior, also a good sign, but one I hope to see continue before declaring improvement is here to stay. This total has bounced around a lot in recent weeks, as benefits expired and were then extended both at the end of 2020, and again in March. The American Rescue Plan Act officially passed into law last month extended benefits to the end of August, so I expect all changes in these numbers to now be actual people truly going back to work, and not just exhausting their benefits.

Big picture: this is really what insured unemployment looks like. Even with the solid drop in continued claims at the end of March, insured unemployment is still solidly in double digits.

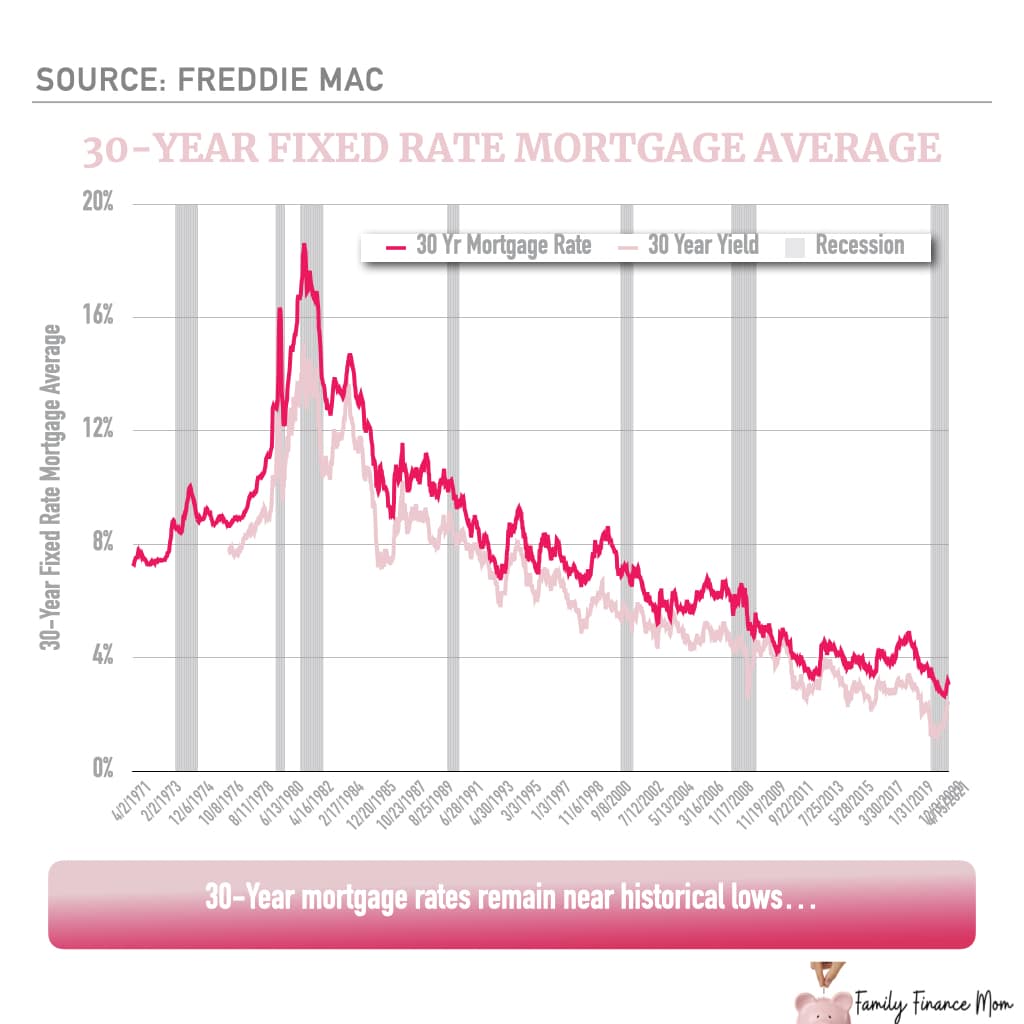

Weekly Mortgage Rates

Let’s chat about mortgage rates… with the housing market on fire, lower mortgage rates continue to support increased demand and make higher priced homes more affordable. Freddie Mac publishes the results from its Primary Mortgage Market Survey every Thursday, giving the weekly US average for 30 Year Mortgage rates. As of 4/15/2021, the average 30-year rate was 3.04% with 0.7 points, but still up +0.37% since the start of the year.

I talk a lot about what’s happening with interest rates – and I’ve included the 30-year Treasury yield on these mortgage charts to help you see how overall market rates truly impact what we pay in interest as well. The 30-year treasury rate is 99.5% correlated with mortgage rates – meaning, as Treasury rates go, mortgage rates do too, almost always. And historically, the spread, or the difference in rate between 30-year treasuries and mortgage rates, has been fairly consistent as well. But note in the second chart, how much the spread has narrowed since the start of the year.

Since the late 1970s, the average spread has been 1.38%… it’s currently only 0.70%. Why? Because the Fed has stepped in as a major buyer of Mortgage-Backed Securities (MBS), holding mortgage rates lower than they might otherwise be. However, recent weeks show their open market purchase activity may be starting to slow.

Lower rates should be a good thing for buyers… but it has an unintended consequence too. The Fed can use open market activities, acting as a large buyer in the market, to lower interest rates, but it can’t force banks to lend at those lower market rates. So while lower rates are making more expensive homes more affordable to buyers, and increasing demand for mortgages, it’s also causing banks to tighten their lending standards. With interest rates very low, banks are less willing to lend to higher risk borrowers, so they limit their exposure by tightening lending standards, limiting mortgage availability to only the most creditworthy of borrowers…. this encourages the Fed to buy more MBS to loosen the credit market, and the cycle repeats itself.

Calling All Realtors & Mortgage Experts…

I will be hosting a second LIVE Q&A this Spring and would love for you to share your expertise and what you are seeing in your local markets as the Spring selling season gets underway.

Sessions:

FRIDAY, 5/14 – 9:30AM ET

If you are able to join, please sign up here!

The Political Update

Congress has begun to start negotiations on a bill to enact Biden’s infrastructure plan. There are two primary issues being debated. First, how to pay for the $1.9 trillion proposal, and two, what actually qualifies as infrastructure. Biden has proposed raising corporate taxes, while most Republicans are concerned that could significantly impeded the economic and labor market recovery currently just underway. Historically, infrastructure spending has been funded by those who benefit from it – like raising gasoline taxes to pay for roads.

Which brings us to the second part of the debate, what actually qualifies as infrastructure? Most Republicans view it as more traditional categories, such as bridges, roads, and rail, while the American Jobs Plan and Democrats are pushing a much broader definition that includes everything from Green Energy and Electric Vehicles to Education and Home Care.

Earlier this month, the Senate Parliamentarian gave Democrats a big win that would allow them to use reconciliation again to pass infrastructure legislation. This would allow them to pass a bill with just 50 votes vs. the filibuster hurdle of 60 votes, given their very slim Senate majority. However, this could also potentially limit what is included in the bill, as it would require them to essentially reopen the budget plan passed in February to add directives to that enact the infrastructure legislation, and only budget impacting items could be included. Senator Joe Manchin, a moderate Democrat from West Virginia, has already expressed distaste for this route.

Another hurdle for the legislation among Democrats also emerged last week. New York Democrats want a repeal of the 2017 SALT cap as part of the infrastructure deal. As part of the 2017 law enacting the “Trump tax cuts,” there was an annual cap of $10,000 put on state and local tax deductions for federal taxes. This negatively impacts residents of high tax states, like New York, where many residents actually felt federal taxes increase despite rate cuts, due to the limit on these deductions, as that might not even represent their annual property taxes, nevermind state income taxes.

We are still likely months away from this proposal getting enacted into law, but will continue to update on its developments as they arise. You can view the full details of Biden’s original infrastructure proposal, known as the American Jobs Plan, In the Market Update from earlier this month here.

The Virus Update

Concerns over a potential 4th wave here in the US continue as the 7-day moving average for new cases has now ticked up +28% nationwide from its mid-March lows. However, it does seem to be slowing late last week. New cases are also now being seen in younger age groups, as most older people are now vaccinated (81% of those over 65 have at least one dose, and 66% are fully vaccinated). On the bright side? More than 50% of Americans over 18 have now received at least one dose of the vaccine.

Experts continue to stress social distancing and masks need to continue to be used until the broader population acheives similar levels of vaccination. Currently, 25% of the total population is vaccinated, 33% of those over 18%.

For going on 2+ months now, we had seen numbers head in the right direction. But post-St. Patrick’s Day, which also coincided with many states rolling back Executive Orders around various health restrictions, there is definitely a visible uptick in new cases. We also for the last 2 weeks have seen an increase in deaths again as well.

Last week also brought the negative headlines around the temporary pause in the use of the J&J vaccine due to a risk of blood clots, seen in 6 women, ages 18-48, out of nearly 7 million doses administered. The pause was out of an abundance of caution. Health officials are scheduled to meet this Friday to determine what warnings or limitations to put on the use of the J&J vaccine going forward.

On the bright side, we do continue to see solid progress in the vaccine rollout. We saw a double-digit percentage increase in both vaccines distributed and administered last week relative to the week prior, and are now vaccinating over 3 million people daily. Note that vaccination data continues to be updated for up to a week, so expect the most recent week’s data to increase. So far, over 84 million people are now fully vaccinated, representing 25% of the population. Many experts believe we need to get to 65-80% vaccinated to achieve herd immunity, which would allow life to resume with some level of normalcy.

The Week Ahead

After a relatively quiet few weeks following the end of March, it’s a big week for economic data as well as the beginning of earnings season. Over 500 companies are scheduled to report Q1 2021 earnings this week (4/19-4/23), including Coca-Cola, P&G, IBM, and Netflix. Stocks were down early Monday due to some negative headlines for Peloton, facing regulatory scrutiny over accidents with its treadmills, and a fiery crash for Tesla that killed two men in Texas over the weekend who were allegedly using the cars autopilot feature.

On the economic front, we also have lots of data coming this week:

- Weekly Jobless Claims

- Mortgage Rates & Fed Balance Sheet data

- Housing market data, including Existing Home and New Home Sales

Ahead of the housing market data release, this week’s deep dive on Finance Explained will talk about the housing market, its current supply shortage, and whether the price increases are here to stay.

For More Information…

For a more detailed history of all the metrics shared, check out When Will the Economy Recover, which I previously updated monthly through 2020, and gives a more detailed overview of market and economic indicators, as well as their historical context.

Questions? Feel free to leave them in the comments below, in the weekly question box in my Instagram stories, or now you can leave me voice messages for the Finance Explained podcast too!