Weekly Market News 3-08-2021

Last week, the market was down more than 1% through Thursday, before rallying on Friday on at least strong headline numbers from the February Employment Report to end the week up 0.8%. Bond yields continued to rise, and mortgage rates crossed 3%, their highest level since last summer. The Senate also passed the $1.9 trillion stimulus bill over the weekend – but what did they have to change to get the votes to pass it? Prefer to listen vs. read? You can now get the weekly headline highlights on Finance Explained, my new podcast. Read on for more of this weekly market news, and you can find all the previous Monday Market Update’s here.

Monday’s Weekly Market News Recap for 03.08.2021

The S&P 500 was down through Thursday, before rallying 2% on Friday to end the week up +0.8%, as Treasury yields continued to rise and inflation concerns persisted. The 10-year and 30-year treasury bond yields are now up 0.64% each since the start of the year, a 70% and 39% increase in yield in less than 3 months.

How does this impact you? It increases the interest rates you pay. Last week, we saw 30 year mortgage rates continue to increase, passing 3%, still near historic lows, but the highest they have been since last summer.

Where are we seeing inflation expectations? A major inflation indicator is the 10 Year Treasury to TIPS spread. Ten-year TIPS yields are currently negative, meaning current actual long-term interest rates are lower than expected inflation. The Treasury spread to TIPS closed the week at 2.21%, another increase from the week prior. The last time the spread was this high was back in 2018, when the Fed was consistently raising the Fed Funds Rate, to offset inflation concerns. This spread historically has predicted inflation growth about a quarter ahead of time, and at current levels, estimates inflation of about 2% for the coming quarter (vs. latest level for January of 1.4%).

Last Week in the Markets

The stock market, absent the 2% rally on Friday spurred by the February Employment Report, would have been the third consecutive week in a row of declines, as long-term treasuries continue to rapidly increase in yield (and decrease in price). Rising inflation concerns are also driving up commodity prices, which continue to dramatically outperform year-to-date, after years of underperformance.

In last week’s stock market, we continue to see tech stocks trail, with outperformance by Small Caps and Value stocks, as investors seek higher returns and dividend yields amid inflation concerns.

In the bond market, you can see a similar outperformance of higher risk securities, as investors seek higher sources of return. High Yield bonds, with lower credit and higher interest rates, have significantly outperformed Investment Grade and Treasury bonds year to date, though all bond indices are now down year-to-date, as rising yields drive prices down. For more on the inverse relationship between bond yields and bond prices, see 10+ Different Types of Investments under How Bonds Work.

Concerns over inflation, and the rapid growth in the money supply, have fueled the rise in more speculative investments, like commodities and cryptocurrencies, like Bitcoin. Want to know more about what’s driving inflation concerns? Check out this post on Higher Inflation.

Bitcoin’s outperformance has been more muted though in recent weeks though, ever since Elon Musk tweeted it might be a little overvalued.

The Economic Weekly Market News

This week’s major economic releases included Weekly Jobless Claims and the detailed Employment Report for February, which came out Friday and is largely attributed as the reason the market rallied. There’s also an update on mortgage rates, as they are the most relevant rate for many family finances and most visibly impacted by rising interest rates in the market.

Weekly Jobless Claims

I continue to closely watch the labor market for signs of improvement, as it has experienced the most negative impact in the economy, and its recovery is most critical to a full economic recovery for everyone. On Thursday, weekly jobless claims for the week ending 2/27 increased to 745,000 from the previous week’s revised level of 736,000. This remains extremely elevated relative to pre-pandemic and even past recession highs. Think about this for a moment: we have had an entire year of weekly claims higher than the highest weekly claims in any prior recession.

Total insured unemployment, under regular state programs, is down to 4.3 million people, an insured unemployment rate of 3.0%. However, this remains a fraction of those covered under the expanded pandemic and emergency programs at both the state and federal level.

Total insured unemployment under these programs for the week ending 2/13 (this comes at a longer lag) is far greater – 18.0 million, but did decline by 1.0 million claims, primarily under the expanded and extended pandemic assistance programs.

The PEUC, or Pandemic Emergency Unemployment Claims, where we see the biggest decline in claims above, is an extension of unemployment benefits for up to 24 weeks after someone has exhausted their state benefits. Both PEUC and Pandemic Emergency UC, as well as additional federal weekly benefits are all scheduled to expire at the end of March and phase out in April. However, the new stimulus bill, passed by the Senate on Saturday, extends these programs through the end of August, as well as expanding the number of weeks of eligibility from 24 to 48.

February Employment Situation

The first Friday of the month is always Jobs Friday – when the Bureau of Labor Statistics releases it detailed Employment Situation report for the month prior. On a headline level, all the numbers were headed in the right direction. Total nonfarm payroll employment rose by 379,000 in February (vs. just 49,000 in January), and the unemployment rate dropped by 0.1% to 6.2%.

But these headlines don’t tell the full story. While there were many job gains in previously hard hit areas, like leisure and hospitality, some sectors saw employment declines, including state and local government, education, construction and mining. Furthermore, we still remain 9.5 million nonfarm payroll jobs short of where we were last year, pre-pandemic.

The headline unemployment rate also understates the real impact of this downturn, as it doesn’t account for the 4.2 million fewer people in the labor force today, than a year ago. The labor force represents people employed and actively looking for work. Today, there are 4.2 million fewer people in the labor force than there were a year ago, and those who have left are disproportionately women. Women represent 2.3 million of the labor force decline or 55% of the total.

If we added those who have left the labor force in the last year into the unemployment calculation, the headline rate would be closer to 9%. The U-6 rate, which includes those who are both underemployed, as well as those who have stopped looking for work in the last year, remained at 11.1% for February, 1.8x the headline rate.

Also while we saw the headline unemployment rate improve for February, it actually got worse for Black Americans (9.9%) and for the least skilled workers, those without a high school diploma (10.1%), and remains far higher for Hispanic Americans (8.5%) as well.

These disparities are now part of the “maximum employment” goal the Fed looks at when setting monetary policy. We saw Fed Chair Jerome Powell speak to Congress two weeks ago and at a Wall Street Journal jobs summit last week where he very clearly reiterated the Fed’s commitment to accommodative monetary policy until the labor market achieves a broad and inclusive level of maximum employment – which given the February data, we still clearly fall short of. On the flip side, the Fed’s accommodative monetary policy is part of what continues to fuel inflation concerns.

For some perspective – we lost more than 22 million jobs in 2 months at the start of the pandemic. It took more than 2 years to lose 8.7 million jobs during the Great Recession, and it took over 4 years to recover them all. We have already recovered 12.9 million jobs since April, which is incredible… but we still are short more jobs than at the worst point of the Great Recession a decade ago.

Do you think women’s employment will increase when schools reopen?

A few of you submitted follow-up questions on Friday around the Employment Report. The impact on women is 2-fold. First, yes, there’s the issue of childcare, which often disproportionately impacts women, and may have led many women to choose to leave their jobs and the labor force to be home with their kids with the closure of schools. But second, the sectors of the economy most impacted by this recession – leisure and hospitality, retail, education and health – are all larger employers of women as well.

An interview last week with new Education Secretary Miguel Cardona, he cited that here in my state of Connecticut, where he comes from and actually toured schools last week with the First Lady, “over 90 percent of the students have an opportunity to learn in person today” already. However, what that number looks like nationwide, and what percentage that is for fully in-person 5 days a week, is not that high.

I think we need schools re-open, 5 days a week, nationwide, as well as fewer concerns that your child could have to quarantine for 2 weeks at a moment’s notice, as well as a recovery in those more women-dominated sectors of the economy to see those 2.3 million women return to the labor force.

Is there a way to measure quality of jobs added? Maybe compensation?

Yes, and yes. The Employment Situation report includes data from employer payrolls, like average weekly hours and average hourly earnings. If we look at this data for nonsupervisory employees, we actually saw both hours and hourly earnings increase at the start of the pandemic, as employment fell. Why? Many of the most impacted sectors are lower wage, with higher part-tine employment. This left higher paid, higher skilled workers on payrolls. It also may have demanded more hours from those who remained on the job.

What do we see with the increase in jobs in February? We saw hours fall slightly, but wages hold, so there may be more part-time employees being added, or less overtime, but not lower paid work.

Is there any tracking of job loss due to Covid-19 vs. just regular firings/job losses?

Not really. At this point, most unemployment is associated if not directly to the pandemic, indirectly from the economic downturn and spillover caused by the pandemic. In February 2020, prior to the impact of the pandemic, the Unemployment Rate was 3.5% with 152.5 million employees on nonfarm payrolls, so that 152.5 million reflects some “normal” unemployment.

For February 2021, we now have just 143.0 million on nonfarm payrolls, so that’s why I think it’s more relevant to look at jobs lost from where we were pre-pandemic. It’s not saying we go back to full, 100% employment – but back to some more normal level of unemployment, which at least historically, has been around 4%.

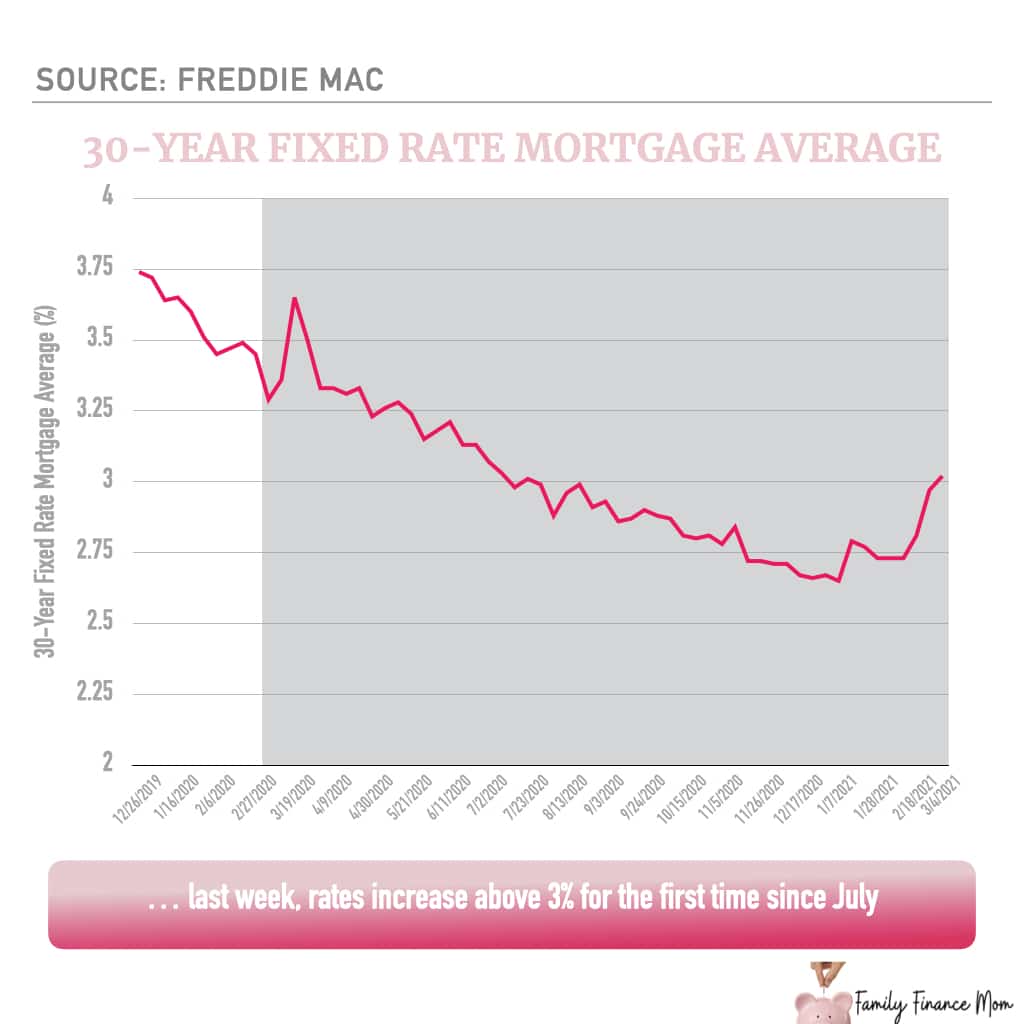

Weekly Mortgage Rates

I have started watching mortgage rates more closely as long-term interest rates have started rising. While mortgage rates still remain at near historically low levels, they are rising weekly as market rates rise more broadly.

Freddie Mac publishes the results from its Primary Mortgage Market Survey every Thursday, giving the weekly US average for 30 Year Mortgage rates. As of 3/4/2021, the average 30-year rate was 3.02% with 0.6 points. You can see how mortgage rates have steadily increased since the start of 2021.

For more on the real estate market, be sure to tune into this week’s special Live Q&A on Friday at 9:30AM ET, where I will be hosting real estate agents from around the country to share what they are seeing in their local markets. I still have a few spots open for real estate agents who’d like to participate. Please sign up at the link below!

Calling All Realtors & Mortgage Experts…

I will be hosting a series of LIVE Q&A’s this Spring and would love for you to share your expertise and what you are seeing in your local markets.

Sessions:

FRIDAY, 3/12 – 9:30AM ET

FRIDAY, 5/14 – 9:30AM ET

If you are able to join, please sign up here!

The Political Weekly Market News

The biggest news on the political front is the Senate voted to pass the $1.9 trillion stimulus bill over the weekend. But it didn’t make it through without some changes to the House version. The House now has to vote to approve the Senate version, which is expected to happen on Tuesday. It will then be signed into law by the President.

Here’s what changed…

Senate Stimulus Bill Changes

The $1.9 trillion package passed by the Senate looks largely similar to the one original proposed by the President, but there were several changes that could directly impact what your family receives in the deal.

- The Senate bill removed the $15 federal minimum wage.

- Weekly federal unemployment benefits will remain at $300/week, as passed in December instead of increasing to $400, but extended to the the first week of September. The Senate bill also made the first $10,200 of benefits people received in 2020 non-taxable for households with incomes below $150,000

- Lastly, they also narrowed the income window for households who will receive the $1,400 stimulus checks. You are eligible if you are single and make less than $75,000, but goes to $0 if you make over $80,000. It’s $112,000 and goes to $0 at $120,000 if you are a single parent, and $150,000 and goes to $0 at $160,000 if you are married, filing jointly.

The Virus Update

While the vaccine continues to be distributed and rolled out nationwide, we still have many months ahead of us of continued precautions… but the trends are solidly headed in the right direction. Nearly 29 million people are now fully vaccinated, and almost 85 million have received at least one dose.

For the seventh consecutive week, we saw all numbers head in the right direction. New cases and hospitalizations all continue to decline. We also continue to see positivity rates below 5%, a solid indicator used by the CDC as a measure of when there are sufficient testing and low community spread, to permit things like schools to re-open.

We also now see a decline in daily deaths as well for the last three weeks. Declines are attributed to a combination of subsiding from the post-holiday spike, as well as the continued aggressive rollout of the vaccine, which began in mid-December.

We also continue to see progress in the vaccine rollout. Bloomberg is tracking the rollout and administration state by state. We saw an 18% increase in vaccines distributed and a 16% increase in vaccines administered last week relative to the week prior. So far, nearly 29 million people have completed their double dose regimen, representing 8.7% of the population. Many experts believe we need to get to 65-80% vaccinated to achieve herd immunity, which would allow life to resume with some level of normalcy.

The Week Ahead

Look for updates on Initial Jobless Claims and 30-Year Mortgage Rates every week. Big news coming up this week? Follow the passage of the revised stimulus bill in the House, expected Tuesday. And since everyone is locked into inflation watch, note the release of the CPI for February on Wednesday morning.

For More Information…

For a more detailed history of all the metics shared, check out When Will the Economy Recover – updated monthly, which gives a more detailed overview of market and economic indicators, as well as their historical context.

Questions? Feel free to leave them in the comments below, in the weekly question box in my Instagram stories, or now you can leave me voice messages for the Finance Explained podcast too!

More to Love from Family Finance Mom…

- How to Learn How to Invest: The 3 Most Important Variables of Investing

- 20+ Awesome Holiday Gift Ideas for Investors

- Financial Truth or Myth: Is A House a Good Investment?

- Is Now the Right Time to Invest in a Home? Expert Insights

- What Drives the Stock Market?

- 3 Ways Diversification in Investing Reduces Your Risk