What Drives the Stock Market?

One of the questions I probably get asked more than any other is why is the stock market behaving the way it is... especially over this last year. The last year has shown to be one of the wildest rides I've seen in the stock market over my lifetime. But its behavior through the pandemic can be explained. If you can understand what drives the stock market, you can explain its behavior from day to day and year to year, based on just a handful of factors. Read on to learn more.

What Drives the Stock Market?

Every day, news comes out that impacts individual stocks and the market as a whole. You can make yourself crazy trying to keep up with its daily whims. But, if you take a step back, and look at the bigger picture over a longer-term time horizon, you can better understand investment risk and what really drives the stock market's performance.

I'm going to break down the stock market's major drivers into two primary groups: fundamental drivers and other, technical drivers. Most investors invest based on fundamental drivers - and look at the market movement created by other, technical drivers as moments that can create buying opportunities.

Let's start with the fundamental drivers... and take a little walk through some stock market history while we do it.

Fundamental Drivers

The stock market is supposed to be a leading economic indicator, driven by expectations of future corporate earnings. A company's share price is supposed to be representative of the future cash flows of the business discounted back to present value by a set discount rate, which is influenced by market interest rates and other investment alternatives. This analysis is thus impacted by a number of fundamental inputs, including company earnings, a company's growth rate, and interest rates.

Robert Shiller is a Nobel Prize-winning expert in economics and behavioral finance, and Yale Economics professor. His Nobel Prize was for his methods of evaluating asset prices. He has researched all types of asset valuations, from stocks to housing (he's also the Shiller of the Case-Shiller Index that analyzes nationwide housing prices). He published much of his research in a book, Irrational Exuberance, that originally was published in 2000, and accurately predicted the tech market bubble. His second edition, published in 2005, accurately predicted the housing market bubble too.

He shares all of his research data on stock market valuation, dating back to 1871, on his Yale home page. I used his data to look at some correlations to the overall market over time to see what fundamental drivers are most correlated to stock market performance.

Corporate Earnings

If we look at the data going back to 1871, corporate earnings are the most correlated driver with market performance. This is followed by Shiller's cycle-adjusted P/E ratio, which looks at earnings over the 10 years prior to normalize for economic cycles.

Over 150 years, as corporate earnings rose and fell, so did the stock market, 90% of the time. But when you look at the data, especially the P/E ratios, does anything about the last 30 years jump out to you?

Interest Rates & Shift to Tech Dominance

The market is constantly changing... and if we look at the more recent, and in particular the modern, more tech dominant market, correlation with earnings has fallen (from 90% to 77%), and other factors have had a greater impact. Specifically, interest rates (from -15% to -63%). Interest rates are negatively correlated with the stock market, meaning they move in opposite directions. When interest rates fall, the market rises, and when rates rise, the market tends to fall.

Over the last 3 decades, the stock market has shifted from one fairly balanced across a range of industries to one increasingly dominated by large, high-growth, tech companies. Back in 1989, tech accounted for just 6% of the weight of the S&P 500. In the 1990s, that weight soared leading up to the tech bubble, reaching a bull market high in March 2000 of 34.5%.

It contracted after the tech bubble burst, but has since ballooned again over the last 20 years. In 2018, S&P made some sector classification changes, splitting real estate out from financials, and moving companies like Facebook and Google from tech to a renamed telecom sector: communication services. If we adjust current numbers to make them comparable to history, at the end of 2020, tech again accounts for well over 30% of the S&P 500.

This shift helps explain, to a degree, why average market valuation ratios, like the market P/E ratio, are so much higher today than history - 1.8x as high over the last 30 years than in the prior 120 years. But this also makes the market more sensitive to interest rates. Tech, which now represents 1/3 of the S&P 500, the most commonly cited index for overall market performance, carries much higher P/E ratios. And valuation ratios are more sensitive to interest rates.

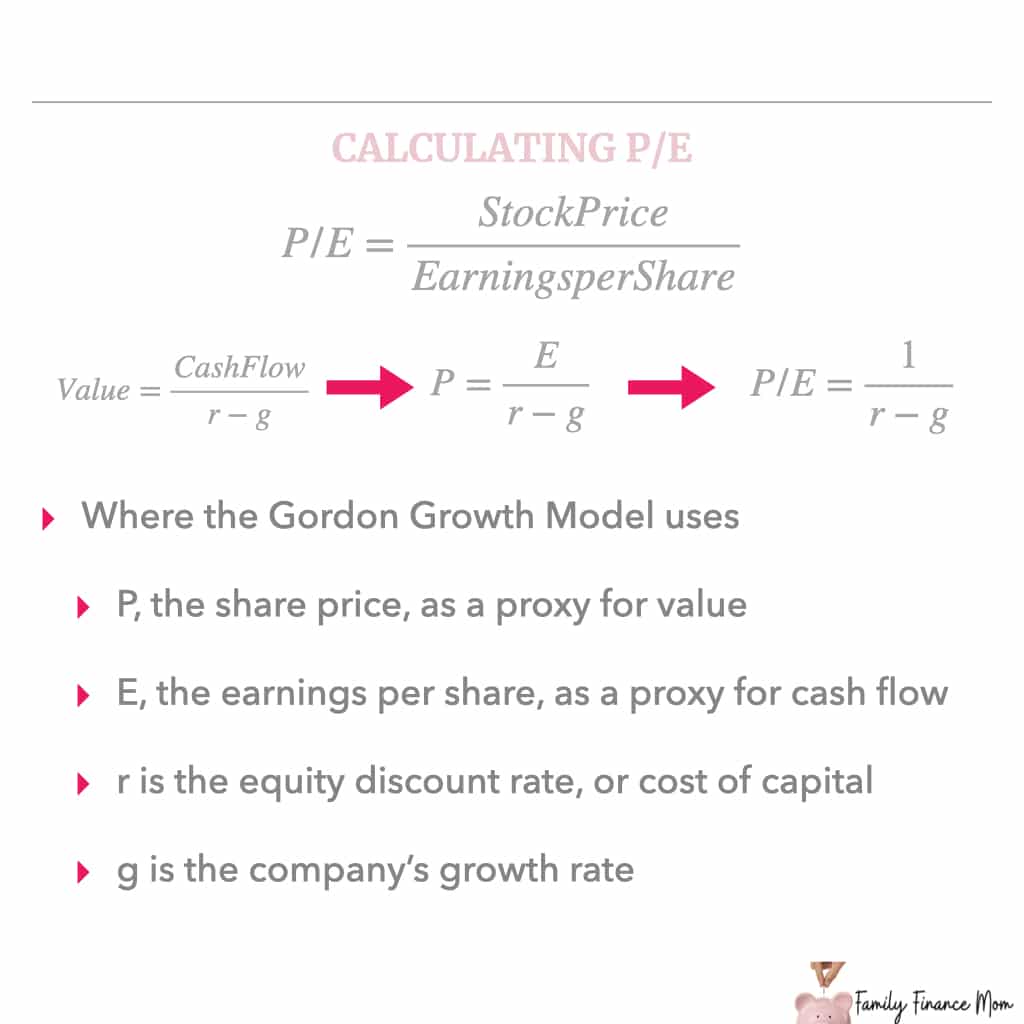

Valuation Ratios

A valuation ratio is simply a comparison between a company's market value, like their share price, to a fundamental financial measure, like earnings. The P/E ratio is the most commonly cited valuation ratio.

In simple terms, the P/E ratio compares a company's current share price to its earnings per share. It can be a backward looking ratio, looking at the reported earnings over the last twelve months, or a forward looking one, comparing current share prices to analyst estimates of earnings for the coming year.

But the P/E ratio (and all valuation ratios really), are actually just a shortcut to more detailed, fundamental financial analyses, specifically discounted cash flows. As an investment analyst, you are trained to analyze financial statements, forecast future company growth, earnings and cash flows, and then discount them back to present value. You can then compare that value to current share prices to decide if a stock is over or undervalued.

A P/E ratio effectively does this in a single multiple, using earnings as a proxy for cash flows. The formula ultimately simplifies to the P/E ratio being equal to 1 over the discount rate minus the growth rate.

The higher interest rates are, the higher the discount rate is and the lower P/E ratios will be. Similarly, the higher growth rate a company has, the more it reduces the denomenator, and the higher the P/E ratio will be.

As an example, if I expect a 20% return on my equity investments, and I invest in a company growing earnings at 15% per year, its P/E ratio should be 1 divided by 20% less 15%, or 20x earnings. If the stock is currently trading at 25x earnings, it is overvalued and not a good investment at the current price. If it is currently trading at 15x earnings, it is undervalued and a good investment at the current price.

High growth, high P/E ratio technology now represents a disproportionate share of the stock market. As interest rates rise and fall, high P/E ratios are more sensitive to these changes, and thus, so are tech company stocks and the market.

Technical Market Drivers

Fundamental drivers are supposed to be what drives the stock market performance. But as with all markets, there are elements of human behavior and competing forces for investors' capital that play a role as well. Technical factors can often cause short-term impacts in the market and are of greater importance to shorter-term investors, while fundamentals drive long-term performance.

Momentum

Momentum traders seek to profit off the herd mentality of human behavior. The general thought is that a stock price on the rise will continue to rise. Sometimes momentum traders also short falling stocks. Momentum investors study stock price charts and moving averages. They look at relative strength, what stocks are outperforming their broader indices, to see what stocks are overbought or oversold, and assume that the trend will continue.

If a fundamental investor is looking to buy low and sell high, momentum investors look to buy high and sell higher. A good recent example of a momentum trade is the performance of GameStop at the start of 2021.

Liquidity

Liquidity is essentially how easily something can be traded in and out of, in order to convert it back to cash. Liquidity can impact the market as a whole, as well as individual stocks.

Smaller stocks with fewer shares outstanding, or stocks that are closely held, with a significant percentage of the stock held by just a few shareholders, can sometimes be negatively impacted, or trade at a discount to their fundamentals due to lack of liqudity.

In the financial crisis of 2008, a liquidity crisis negatively impacted the market as a whole. With losses mounting in the financial sector due to spillovers from bad mortgages and even worse derivative bets on bad mortgages, investors looked to generate cash wherever they could - including by selling off stocks. While much of the negative fundamentals were isolated to the housing and financial sectors, the lack of liquidity caused negative impacts across the stock market and other investment markets too.

Some argue that the multiple rounds of stimulus checks and the significant increase in the money supply over the last year has created excess liquidity... it's driving higher inflation concerns, as well as fueling excess stock market demand, driving up the stock market price and detaching market performance from actual fundamentals.

What's Driving the Current Stock Market?

Now that you have a better sense of what drives the stock market historically, let's examine what's driving the current stock market. Every Live Q&A I get asked if there's a stock market bubble or if the stock market is going to crash soon.

The current market continues to be driven by two competing forces:

- Stock market rallying on hopes of economic (and corporate earnings) recovery

- But tempered by rising interest rates fueled by inflation concerns

... and currently, historically low interest rates have driven valuation ratios near record highs, even on a cyclically adjusted basis. The only period when Cyclically Adjusted P/E Ratios surpassed currnet levels was in the late 1990s, pre tech bubble burst. They peaked at 44x earnings in December 1999. This is what's fueling some of those bubble concerns. But interest rates today are also far lower than they were in the late 1990s - just 1.67% vs. over 6%.

Rising interest rates have a greater effect on the market today, than they did historically, as they reduce valuation ratios, especially for high multiple tech stocks. Note how tech stocks have underperformed year-to-date, as interest rates increased.

Over the last year, the stock market as a whole rallied from its pandemic-low, on the expectation that corproate earnings would recover - that the impact of the recession would be temporary. Starting this week, we now enter Q1 2021 earnings season... and many investors will expect to see signs of recovery in earnings as well as in the outlook shared by executives this earnings season.

If interest rates rise, lowering valuation ratios as actual earnings materialize in the economic recovery, we may not see a major market correction. Though many do expect below average market growth for the coming years from current market levels.

However, if we don't hear positive signs of recovery and solid earnings growth expectations from corporate executives over the next 2-3 weeks of Q1 earnings season, the market could definitely be in for a bit of a bumpy ride.

How do you feel about the current stock market? What other questions do you have about the current stock market performance? To track how these drivers move over time, be sure to follow my weekly Market Updates here. You can also listen to them via my podcast, Finance Explained.

Spread Financial Literacy! PIN THIS!

[…] Mid and long-term bond yields peaked at the start of April, before starting to soften over the last several weeks. Just that little bit of softening, mostly due to investors’ beliefs that the Fed will hold off on raising rates for now, which the Fed reaffirmed following its regularly scheduled FOMC meeting last week, takes some headwind pressure off the stock market. To better understand the relationship between interest rates and the stock market, check out What Drives the Stock Market? […]

[…] Mid and long-term bond yields peaked at the start of April, before starting to soften over the last several weeks. Just that little bit of softening, mostly due to investors’ beliefs that the Fed will hold off on raising rates for now, which the Fed reaffirmed following its regularly scheduled FOMC meeting last week, takes some headwind pressure off the stock market. That sentiment changed this week, with the CPI report revealing solid year-over-year prices increases. To better understand the relationship between interest rates and the stock market, check out What Drives the Stock Market? […]

[…] Mid and long-term bond yields peaked at the start of April, before starting to soften over several weeks. Just that little bit of softening, mostly due to investors’ beliefs that the Fed will hold off on raising rates for now, which the Fed reaffirmed following its regularly scheduled FOMC meeting last week, gave the market room to run over the first few weeks of April. However, last week, interest rates began to increase again and stopped the stock market’s progress. To better understand the relationship between interest rates and the stock market, check out What Drives the Stock Market? […]

[…] Related Post: What Drives the Stock Market? […]

[…] general, raising taxes on corporations directly reduces future company earnings. Stocks trade based on expectations of future company earnings, so this proposal, if passed, would negatively impact trading values. Higher taxes on investment […]

[…] To better understand this relationship between the stock market, company earnings, valuation ratios and interest rates, be sure to check out 5 Factors that Drive the Stock Market. […]

[…] To better understand this relationship between the stock market, company earnings, valuation ratios and interest rates, be sure to check out 5 Factors that Drive the Stock Market. […]

[…] To better understand this relationship between the stock market, company earnings, valuation ratios and interest rates, be sure to check out 5 Factors that Drive the Stock Market. […]

[…] putting such downward pressure on the market? Recall the major drivers of stock market performance include interest rates and company earnings. The stock market is inversely correlated […]

[…] Related Post: What Drives the Stock Market? […]