Where To Invest Money: ETFs vs. Mutual Funds vs. Index Funds

In our current crazy, economic environment, I've been hosting a daily LIVE Q&A on Instagram every weekday at 10AM ET. One question I've been asked over and over and over again goes something like this: "Should I invest in an Index Fund or a mutual fund?" or "ETF or Index Funds - which is better?" People want to know where to invest money... so let's talk about the different options, the correct comparisons to be making, and help you make an informed decision about where to invest money based on your family's financial goals and objectives.

Where To Invest Money

With the market in decline, and big investors making moves, many of you are eager to invest as well. I frequently get asked about index funds vs. ETFs, or mutual funds vs. index funds, but both of these questions make the wrong comparison. It's like comparing apples and oranges, or more accurately, comparing the fruit salad to the salad bowl.

So where should you be putting your money? And what are the right questions to answer? When deciding where to invest money, you really face three different questions:

- What's the right investment account

- What's the right investment vehicle

- What's the right investment strategy

So, let's examine each one of these to help you make the best decision on where to invest your money given your specific goals and investment objectives.

What Investment Account Should You Use

You often hear me say, there's no one answer for everyone. And the same applies to all of these investment questions as well. When you are trying to decide where to invest money, you first have to get your money from your checking or savings account into an investment account that allows you to invest in securities and investment funds.

Before choosing an investment account, you really need to know your family's financial goals and what you are hoping to invest to achieve. Why? Because there are tax-advantageous investment accounts for different goals. And not having to pay taxes on gains every time you trade or re-balance your portfolio means your funds will grow faster and compound, uninterrupted.

Related Post: What's the Best Way to Invest When You're Just Getting Started

For retirement, use your 401k or 403b offered through your employer. If that's not an option, or you max it out and want to save more, look at IRAs. You can open an IRA with any major brokerage. I have mine at Fidelity, but there are lots of options out there. Be sure to consult the IRS website each year for annual contribution limits, as well as income limits if you are using a Roth IRA.

For college or education savings plans, consider using a 529 Plan. It functions much like a 401k, though contributions are not tax-deductible for federal taxes.

Related Post: The Best Way to Save Money for Kid’s College

Once you've exhausted tax-advantageous investing options, or if you will need to use the funds before you plan to retire, you may choose to invest from a taxable brokerage account.

What Investment Vehicle Should You Use

Once you have your money in an investment account, it's time for the next choice on where to invest money. Do you want to buy individual stocks and bonds directly? Or would you like to invest in a pooled investment vehicle, that offers you greater diversification, like an ETF or mutual fund?

Related Post: Investing in Stocks 101: 10 Things To Know About a Stock Before You Buy One

It is important to know that some investment accounts may limit where you can invest your money. From a brokerage account and most IRAs, you can invest in just about anything. But for other tax-advantaged accounts, like in a 401k or 529 Plan, you will likely be limited to a pre-established set of mutual funds offered by the plan administrator.

Either way, it is important to understand the different investment options and how pooled investment vehicles, like Mutual Funds and ETFs, work. Let's take a look at what an ETF is, what a mutual fund is, how they are alike and how they are different, to help you decide where to invest money based on the best fit for you and your goals.

What is an ETF?

ETF stands for Exchange Traded Fund. An ETF manager (known as a sponsor) files a plan with the SEC to create an ETF. Then, and this is a bit oversimplified, the manager places assets in a trust, divides the trust into shares, and those shares are then sold to the public on the open market, much like stock shares in an IPO.

The fund may be invested in stocks, bonds, other marketable securities, and even other ETFs. The manager can follow any number of different investment strategies, but the vast majority of ETFs are Index Funds. More on that in a moment.

As their name implies, an ETF trades on an exchange, and is priced in real-time when the market is open. The minimum to invest is the price of 1 ETF share, which can be as little as $50 or as high as several $100, but often significantly less than the investment minimum for a mutual fund. When you buy an ETF, you are likely buying on the secondary market, buying an ETF share from someone who is selling it.

ETFs were first created in 1993, so they have only been around for a few decades. But they have seen significant growth, and investors find them attractive given their ease of trading and lower entry cost. According to ICI, as of the end of 2019, there were $4.4 trillion invested in ETFs in the US.

What is a Mutual Fund?

A Mutual Fund is a pooled invsetment vehicle made up of money from many different investors and managed by a professional money manager on their behalf to a specific investment strategy. Like an ETF, the fund may be invested in stocks, bonds, other marketable securities and even other mutual funds or ETFs. A mutual fund may be managed as an index fund, but most mutual funds use more actively managed investment strategies.

Unlike an ETF which trades on an exchange and can be purchased at a set price whenever the market is open, mutual funds are only purchased once a day, at the market close, at a set Net Asset Value (NAV). Everyday, a mutual fund calculates its NAV by adding up the current value of all the stocks, bonds and other securities (including cash) in the fund's portfolio and then dividing the total by the number of shares in the mutual fund.

To buy into the mutual fund, you buy in at the current NAV. Your cash gets added to the fund and invested along with everyone else's. Given this process, mutual funds have investment minimums, which require you to buy in at a minimum initial investment, usually several $1,000s, which may add up to a number of shares. Once you've met this minimum, you can invest in smaller increments going forward.

Mutual funds date back to the 1920s. Many of the assets in mutual funds are from retirement funds. They are an attractive option if you wish to automate and repeat specific transactions, like, add $500 to your IRA every month and invest it 3 specific mutual funds.

How to Choose ETFs vs. Mutual Funds

So which should you choose? It ultimately depends on what you are looking for. If you want to invest with a lower initial investment minimum, an ETF is a better option. If you are looking for more of an automated way to invest, get the minimum invested in a mutual fund, and then set it up to invest a certain amount every month.

And remember, certain investment accounts, like 401k's and 529 Plans, often only give you a pre-determined set of mutual funds to choose from, typically all managed by the plan administrator.

More About Investing from Family Finance Mom

Build your knowledge and confidence to start managing your family's investment portfolio!

How to Choose the Best Investment Accounts for Beginners

Want to start investing but not sure where to begin? It starts with choosing the right investment account. Here's what you should know about your options

What's the Best Way to Invest Money (When You're Just Getting Started)

The first thing you need to start investing? An investment account. Understand your options and the place to get started

10 Things to Know About A Stock (Before You Buy One)

Learn the 10 things you should analyze about any stock before you buy it to help you determine if it's a great business at a good price. FREE downloadable spreadsheet to analyze your stocks

10 Questions To Ask A Financial Advisor Before Hiring One

Ready to get some help with your investment portfolio? Here's what you'll want to ask a Financial Advisor in your intro meeting BEFORE you make the decision to hire one

Understanding Investment Risk for Women

Women are more risk-averse than men. But when we do invest - we actually outperform them! The better you understand investment risk, the more likely you are to invest...

4 Major Economic Indicators Families Should Follow

Are we headed for a recession? Understand these 4 leading, major economic indicators, and how they signal where we are in the economic cycle to make better financial decisions for your family

What is a Lagging Economic Indicator?

Only lagging economic indicators can CONFIRM a recession. Here are the 4 major ones to watch to track the economic cycle.

What Investment Strategy Should You Use

Now that you have your money in an investment account, and you've chosen the investment vehicle you prefer, you have one last question to answer. Where to actually invest your money.

If you decided to invest in an ETF or a mutual fund over individual stocks and bonds you choose yourself, you'll need to choose what kind of investment strategy you prefer. Investment strategies can generally be broken into two main buckets: passive strategies, like Index Funds, and active investment strategies.

Index Funds vs. Active Investment Strategies

As their names imply, a passive investment strategy is more automated, with managers investing the fund to replicate a defined index, like the S&P 500. Hence the name, Index Fund. Standard and Poors publishes the stocks in the S&P 500 and their weights, and the Index Fund manager just has to trade to replicate it.

Active investment managers do a lot more work and research to invest the assets in their portfolios. They may be stock or bond pickers (like my old job as an Equity Research Analyst), choosing the companies they think will outperform expectations, or they may design complex computer programs based on all sorts of data feeds to pick investments. This takes more man-power, more resources, more time, and they charge higher fees to cover those costs.

Morningstar, the leading mutual fund research firm since the 1980s, publishes a semi-annual report, the Active/Passive Barometer. It measures how many actively managed funds beat their passive peer for their category. For example, does an actively managed large-cap equity fund beat an S&P 500 Index Fund?

In any given time period, typically fewer than half of active managers outperform their passive peers. Over longer time horizons, it's even less. According to Morningstar, only 23% of all actively managed funds topped the average of their passive rivals over the last 10 years. This is even more true for large-cap funds, with active managers doing slightly better in small-cap, foreign stock funds, and bond funds.

It begs the question - if the actively managed funds don't beat their benchmark, why are you paying them higher management fees to invest your money when you could pay a lot lower fees and just invest in an index fund?

Investors have wised up. The outperformance of passive strategies, like index funds, versus more actively managed strategies, combined with their lower fees, has driven more and more investors toward index funds over the last 10 years.

Investment Fee Considerations

When you invest there are different fees you have to consider which impact your investment returns as well. When you buy individual securities, stocks or bonds, you will pay trading commissions, both on the initial purchase and when you sell your investments. These trading commissions also apply to buying and selling ETFs. With many brokers, these are often a fixed fee, like $4.95/trade, no matter whether you are making a $10,000 trade or a $100 one.

Then, both ETFs and mutual funds will have a published expense ratio. The published expense ratio includes management fees, other expenses, and in the case of mutual funds, may also include distribution fees. These are fees paid to investment advisors for selling you the funds. ETFs do not have distribution fees, but keep in mind you pay trading commissions when you buy and sell your ETFs.

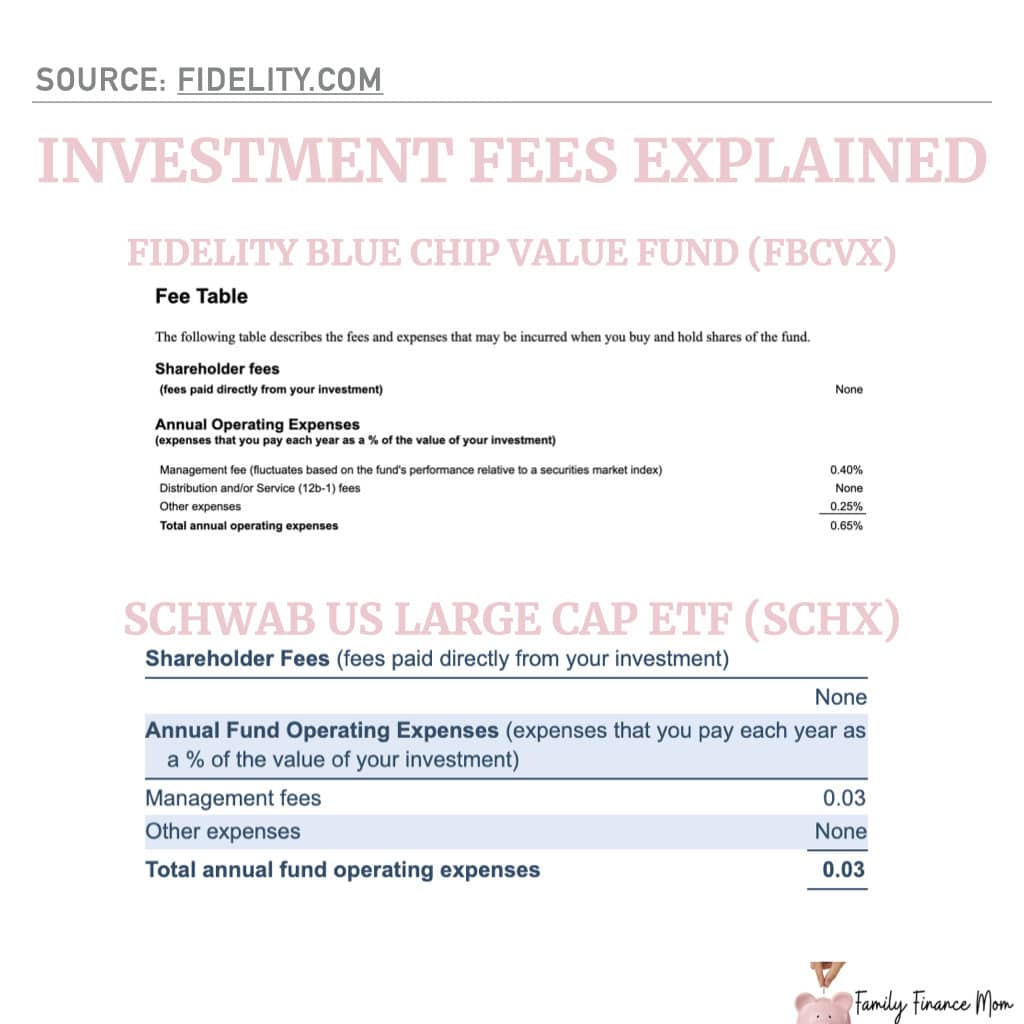

For the two examples above, the Fidelity Blue Chip Value Fund (a large-cap equity fund) has an expense ratio of 0.65%. Every year, you will pay 0.65% of the money you invest in the fund in fees. The more passively managed, Schwab US Large-Cap ETF (also a large-cap equity fund), has an expense ratio of 0.03%. There are no distribution fees.

According to Morningstar's annual US Fund Fee Study, both actively managed funds and passive funds have seen fees decline over the last several years. This is due to both increased interest in passive funds, which are lower fee, and increased competition among fund managers looking to gain more investors.

The table below, also from the April 2019 Morningstar US Fund Fee Study, shows how fees vary by investment strategy more granularly. In general, you should expect to pay higher fees for actively managed funds, fund with less liquid investments, and for funds with lower assets overall, as there are fewer assets to spread the costs over.

Lower fees mean less of your money going to an investment manager's profit and more of your money stays invested to compound and grow year after year. And if 77% of active managers don't beat the passive index over the long run anyway, why are you paying them to try?!? I can almost guarantee that as average investors, we have less ability to pick the small fraction of managers who do beat the index than the average investment manager does to pick stocks that beat the market.

Return Potential

Now, the last big question... what about the investment return?

The more risk you are willing to take, the higher your expected return potential. And historical data bears that out. The chart below depicts risk vs. annualized return since 2000 for a large-cap index (S&P 500), a small-cap index (Russell 2000), a growth index (Russell 1000 Growth Index), and a value index (Russell 1000 Value Index).

Risk is measured by annualized volatility, or how much the returns vary from year to year, up and down, relative to the average. The size of the dot is an estimate of the number of assets invested in index funds like these based on ETFs at the end of 2019.

If you want slow and steady, with less up and downs along the way, lean towards large cap equity funds. If you are willing to take a little more risk, you can earn higher returns.

Note, over the last 20 years, we have experienced 3 major stock sell-offs, in 2001, 2008, and are in the midst of one currently, resulting in the lower than expected annualized returns you see in the chart above.

Fund options are typically characterized by the following, or some combination of the following, terms:

- Blue Chip - invested in the largest market cap companies, like stocks in the Dow Jones Industrial Average (top 30)

- Large Cap - invested in large market capitalization companies, like stocks in the S&P 500 (top 500)

- Small Cap - invested in smaller market capitalization companies, like stocks in the Russell 2000 (smallest 2,000 stocks out of the top 3,000 stocks in the US)

- Value - stocks with solid fundamentals (revenue, earnings, cash flow), priced below its peers based on comparable valuation metrics

- Growth - stocks with fundamentals (revenue, earnings, cash flow) growing at a rate faster than its peers

- Blend - includes both growth and value stocks

- Aggressive - takes risk (volatility) greater than that of the broader market to generate returns greater than the market

- Moderate - takes risk (volatility) in line with that of the broader market to generate returns in-line with the market

- Conservative - takes risk (volatility) less than that of the broader market and generates returns below the market

- Target Date - a fund of funds that shifts the mix of stocks and bonds in your portfolio appropriately as you age (more stocks when you are younger, more bonds as you approach your target date)

What other terms have you seen in ETF and mutual fund names that you would like to see explained?

Hopefully, now you feel more confident choosing where to invest money. Put it into the right investment account for your goals, be they retirement, early retirement, college savings, or just to invest. Then, pick the investment vehicle that best meets your objectives, and the investment strategy that best meets your return and risk preferences.

More questions about investing? Come ask me during my LIVE Q&A on Instagram - every weekday at 10AM ET.

Ready to Invest? PIN THIS for later!