Why the National Debt Matters: Understand Your Family’s Risk

Learn why the national debt matters and how it directly impacts your family now, and going forward

We all have our biased lens through which we look at the world. As a former financial analyst, my lens is biased towards the numbers: dollars, cents and statistics. While today there are many points of highly publicized political debate, no matter your side of the fence or feelings about our current President, I believe no single issue can threaten our collective economic future more than the ever-growing national debt.

Note: this post was updated as of 4/27/2020.

Why the National Debt Matters

For some of you, you hear the words debt, deficit, government spending, or GDP and your eyes start to glaze over. You might think that the US government has plenty of money. That it can just print more money if it needs to. Or that this does not affect my family on a daily basis. But the truth is it actually already does. Here’s why the national debt matters.

US Spending Exceeds Revenues… Every Year

The US government’s current level of spending, relative to both the size and growth of our economy, as well as current tax revenues is unsustainable. To support it, the US must take on more and more debt every year (even raising taxes to 100% on the wealthiest won’t cut it) – raising money from large investors, primarily your future retirement funds, and foreign governments. This is just with regular government spending, existing commitments, and entitlements. Economic downturns and stimulus spending, only add to the debt pile.

It must also pay interest on all the debt outstanding, adding to its annual expenditures and displacing other necessary government expenditures like healthcare, social security, education and national security. And the impact is happening already. For the last fiscal year, net interest expenditures were over $375 billion, more than 2x what the federal government contributes to education!

National Debt Facts

First, a few national debt facts…

As of today, the national debt is nearly $25 trillion. To put that in a little bit more tangible perspective, that amounts to over $75,000 per US citizen and nearly $200,000 per US taxpayer. That total also does not include an additional $1.2 trillion and $2.1 trillion in state and local debts.

It is also well over 100% of US GDP, or the total amount of ALL goods and services produced in the country in a given year. This measure, known as the debt to GDP ratio, is generally considered to indicate the health of a country’s economy – ratios over 77% for an extended period of time are generally considered to be harmful for growth.

Note that we surpassed 77% in the early 2000s, and have not seen Debt to GDP ratio levels this high since post-WWII. Those debt levels came about due to war-time spending and receded as veterans returned to the home front, went back to work, and the economy boomed.

Debt vs. Deficit

You may hear people talk about the national budget deficit. A deficit is the amount of spending over your income. If you make $4,300 a month (indicative of the US median household income), but spend $5,000 a month on expenses, you have a monthly deficit of $700. Every month you have to find some way to fund that deficit – typically through debt. Whether you put it on a credit card or draw on a home equity loan, at the end of the year, you will have accumulated $8,400 in additional debt.

For simplicity’s sake, the US government is no different . Every year that it spends more than it collects in taxes, it has a national budget deficit that must be funded with debt. In FY2019, the US government spent more than $4.5 trillion, with a $984 billion deficit funded by adding to the national debt.

Good Debt vs. Bad Debt

One more point of financial fact. Not all debt is bad. Most households in the United States carry debt – be it a mortgage, small business loan, auto loan, student loans or credit card debt.

Debt that fuels investment and supports growth is generally good financially speaking. When the cost of debt (the interest you pay) is lower than the expected growth or return, that is a good financial decision. Home mortgages, small business loans, and student loans generally fall in this bucket. If you take out a small business loan to expand your business, hire new employees, and produce more income, you will be able to pay the interest on, and ultimately pay off, your debt.

Learn More About Debt

Want to better understand debt, how it works and the impact debt has on your family finances? Check out these posts on DEBT.

What is Good Debt Versus Bad Debt?

What is the impact of debt on your finances - and when is it okay to use debt? What makes debt good or bad?

The Ugly Truth About Student Loan Debt

The reality of college and the impact of student loans on your financial future.

More from Family Finance Mom on College and Student Loans

Learn more about the cost of college, how to pay for it, save for it (529 plans), and the impact of student loans.

Debt that is necessary to support ongoing, recurring expenditures without any expected future growth is not good. If you are spending more than you make every month, and maxing out your credit cards to support your spending levels, that is not sustainable. Every month, more of your income will be spent on interest, with little ability to pay off your debt and likely the need for even more debt every month, creating a vicious, downward financial spiral.

Currently, the government is funding more than 22% of its annual spending, spending that is largely recurring in nature, fulfilling outstanding commitments and obligations, that are unlikely to generate future growth, with debt.

Why the National Debt Matters

So now that you better understand the terminology and where we are at today, let’s go back to why the national debt should matter to you, both now and going forward. There are entire semester long courses in Macroeconomics that study this, but I will try to focus on why the national debt matters as it pertains to parents raising families in today’s America.

How much does the debt cost?

The current average interest rate across outstanding US debt is approximately 2.29% (as of March 2020). This drove 8.4% of government expenditures on interest in the FY2019.

For the last decade, we have lived in a persistent, low-interest-rate environment. Ten years ago, the average interest rate across outstanding US debt was more than double current rates, at over 5%. And as recently as 2000, outstanding Treasury Bonds paid interest over 8%. The chart below depicts the net interest expense on today’s national debt balance at varying interest rates, and resulting annual deficit, assuming no changes to government spending.

If interest rates returned to 8% on current national debt balances, the government would have to spend over $1.2 trillion on net interest and create an annual deficit of nearly $1.8 trillion, almost double the current annual deficit.

As interest rates rise (which can happen when 1) the economy improves and 2) if the country’s credit risk is deemed to be greater), government spending on net interest on the national debt also rises. This will either be funded by raising taxes on all Americans, with more debt (at ever-higher interest rates, creating a vicious cycle), or by cutting other government expenditures in areas your family likely depends on, like Pensions, Healthcare, Defense and Education.

How does the National Debt Impact Other Public Spending?

The national debt already impacts other public spending. Many in Congress recognize the dangerous levels of debt the country already carries. They seek to limit new legislation that adds to the deficit. Many of the protests against universal healthcare were because of the significant increase in deficit spending it creates, without any real addressing of the exorbitant, ever-increasing costs of healthcare.

In education – where the US spends more per student than any other country in the world, while producing below average results – legislators question increasing federal funding for education without accountability for end results.

Legislators can pass all kinds of legislation that makes great headlines, but for it to actually become a reality, it has to also be granted funding. When budgets are already under tremendous pressure, programming is cut, reduced or goes completely unfunded.

Legislation for good programs stalls or goes nowhere. Most people agree that taking on more debt is not a good thing at current debt levels, without a plan going forward to reduce spending, reduce overall debt levels and increase economic growth and GDP, all of which would reduce the key debt to GDP ratio.

Where Does the Money Come From?

For the government to raise money through debt, someone has to be willing to buy it. US treasuries are issued as bills, notes and bonds. These vary in terms of maturity, or how long they will remain outstanding. Just like you can take out a mortgage for 10, 15 or 30 years, treasury bills typically have maturities less than 1 year, notes two to 10 years, and bonds 10 to 30 years. The longer the maturity, typically, the higher the interest rate.

Related Post: Why Interest Rates Change

However, unlike a mortgage where you pay interest and principal every month, the government only pays interest until the debt matures – then, they must pay it off, with cash or by raising more debt to replace it. So the debt currently outstanding is constantly maturing and being reissued. If existing holders ever elect to not reinvest in US treasuries, the government’s ability to retire and reissue debt will become increasingly difficult and/or more expensive.

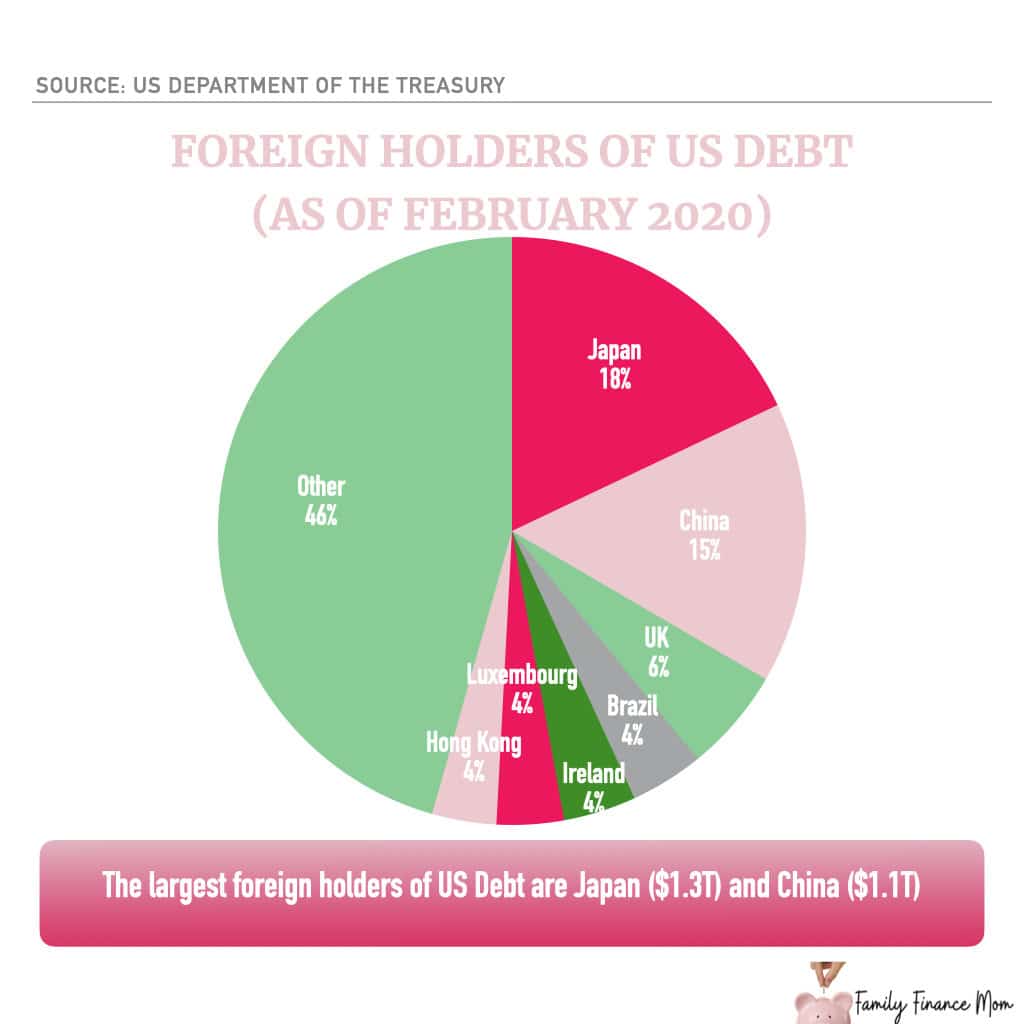

Currently, US debt is held by both various government agencies (called “intragovernmental holdings”) and by public holders. Roughly one-third is held by foreign governments.

Japan and China are the largest foreign holders, holding more than $1 trillion each in US treasuries. They have a vested interest in supporting US treasuries to insure the US dollar remains strong, and Americans buy their exports.

Prior to researching this post, foreign ownership was my biggest concern. But far more concerning to me now is the balance of ownership.

One quarter of the national debt is held by ‘intragovernmental holdings,’ which primarily represents retirement funds from Social Security (nearly $3 trillion) and federal government and military personnel (nearly $2.0 trillion). Of the remaining other public holdings, much of that is from mutual funds, state and local pensions and private pensions. Therefore, the majority of the national debt is currently held by American retirement funds.

If the US government ever defaults, or even if their debt is downgraded and the face value has to be discounted, billions of retirement funds for millions of Americans goes with it. Or what will happen as Social Security can’t meet its unfunded liabilities and has no excess cash to purchase US Treasuries?

Remember when mortgage-backed securities brought down multiple major Wall Street banks??? It’s potentially quite the house of cards.

Learn More About Why the National Debt Matters

I’ve addressed your questions about the national debt on a couple daily Live Q&A sessions already. You can catch those replays about why the national debt matters and how it impacts us all here:

$25 trillion is a hard number to grasp. It is more than the entire country – all businesses and individuals combined – produces in goods and services in an entire year. That alone should be enough cause for concern, but the pressure the national debt puts on other government spending, the ongoing interest expense, and the massive amount of American retirement funds supporting, it should raise serious alarm bells.

And this doesn’t begin to touch on the more than $100 trillion in unfunded liabilities – representing future commitments already made by the government which will come due for Social Security, Medicare, and retired Federal and Military benefits.

This is a complex topic, but one that deserves the attention of all American families. You can explore the concept of the National Debt more with your kids with this resource from the US Treasury, Treasury Direct Kids. Learn more about the history of the National Debt, track the daily national debt, play games and more.

Sharing is caring: PIN THIS!

[…] Related Post: How the National Debt Impacts YOU […]

[…] Related Post: Why the National Debt Matters […]

[…] Related Post: Why the National Debt Matters […]

[…] years, and really more like decades, people have been raising concerns over the national debt rising. Today, however, those concerns have become a much more certain reality. What makes now […]